Financing the Future: A Matriculant's Guide to Scholarships, Bursaries, and Loans

As a Grade 12 learner, your mind is currently processing a massive multi-variable equation. You are balancing trial exam prep, calculating your Admission Point Score (APS), and trying to decide what to study next year.

But there is one massive variable that many matriculants leave until the very last minute: How are we paying for this?

Higher education in South Africa is an incredible investment, but it comes with a price tag that can look intimidating. Fortunately, there are billions of Rands floating around the tertiary ecosystem designed to fund students. The trick is knowing how to decode the terminology. Many learners use the words "bursary," "scholarship," and "student loan" interchangeably, but they are entirely different functions with very different repayment equations.

In the ancient root of algebra, al-jabr means "the restoration of balance." Let's clear up the confusion and map out the ultimate South African tertiary funding matrix.

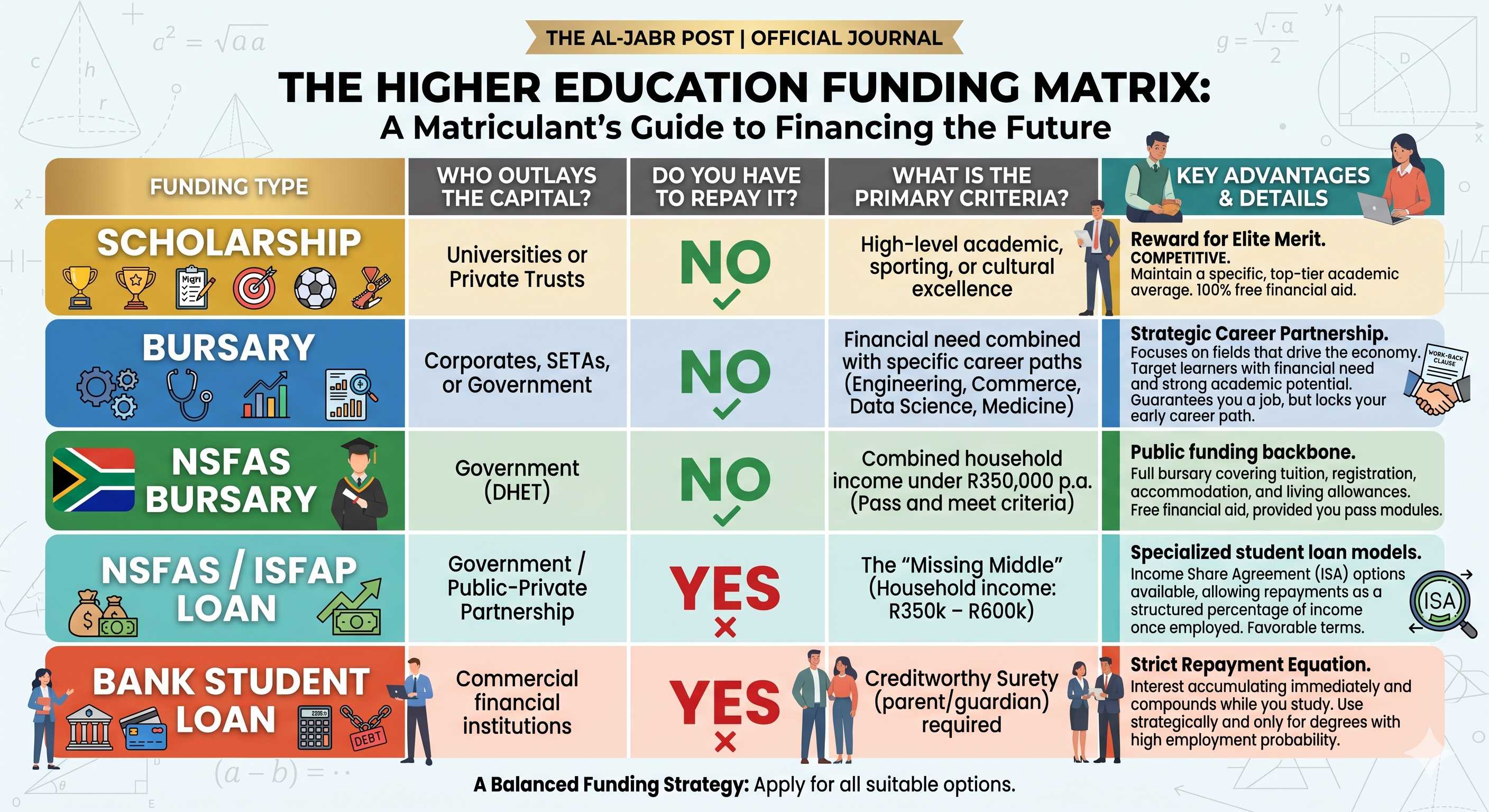

1. Scholarships: The Reward for Elite Merit

Think of a scholarship as an investment in your raw academic or extracurricular talent.

-

The Reality: Scholarships are rarely awarded based on how much money your family makes. Instead, they care about your performance variables. If you are a straight-A student, a national-level athlete, or a virtuoso musician, private foundations or universities will compete to fund you.

-

The Fine Print: They are highly competitive. Furthermore, they usually require you to maintain a specific, top-tier academic aggregate (e.g., keeping a 75% or 80% average at university) to stay funded each year.

2. Bursaries: The Strategic Career Partnership

A bursary is typically a corporate or institutional agreement. Companies don't give bursaries out of pure charity; they give them to build a pipeline of future talent for their industries.

-

The Reality: Bursaries focus heavily on fields that drive the economy—like Engineering, Commerce, Data Science, and Medicine.

-

The Work-Back Clause: This is the most critical variable to understand. Many corporate bursaries feature a "work-back" contract. This means that if they pay for your three-year engineering degree, you legally agree to work for that company for three years immediately after graduating. It’s a massive win because it guarantees you a job, but it means your early career path is locked in.

3. NSFAS & The "Missing Middle" (Grants vs. Loans)

The National Student Financial Aid Scheme (NSFAS) and programs like the Ikusasa Student Financial Aid Programme (ISFAP) form the backbone of public funding in South Africa. The funding structures adapt based on your family's financial threshold:

-

The NSFAS Bursary (Under R350,000): If your combined household income is under R350,000 per year (or under R600,000 if you live with a disability), NSFAS acts as a full bursary.

-

The "Missing Middle" Loans (R350,001 to R600,000): If your parents earn too much to qualify for a full NSFAS grant, but too little to afford university fees or secure massive bank loans, you fall into the "missing middle."

-

The Income Share Advantage: Innovative pilots in the missing-middle funding space (like ISFAP's partnership with Chancen) utilize Income Share Agreements (ISAs).

4. Commercial Student Loans: The Strict Repayment Equation

If you do not qualify for a merit scholarship, a corporate bursary, or government assistance, commercial banks (like Standard Bank, FNB, Absa, or Nedbank) are an alternative option.

-

The Reality: A bank loan is a strict commercial contract. To get one, you need a parent or guardian with a good credit score to sign as a surety (meaning they promise to pay if you can't).

-

The Interest Trap: Unlike government options, interest begins accumulating immediately. Typically, your parent will need to pay off the monthly interest while you study, and the moment you graduate, you take over the full monthly repayments for the principal debt. Use this option strategically and only for degrees with high employment probability.

Balancing Your Funding Strategy

Do not make the mistake of applying to just one funding pool. Treat your applications like a balanced probability equation:

-

Apply for NSFAS early as your primary baseline if you fall within the income thresholds.

-

Look up corporate bursaries specific to your chosen field of study.

-

Keep your Grade 12 marks as high as humanly possible to trigger automatic university entrance scholarships.

At The School of Mathematics, we know that high final marks are the ultimate leverage when applying for financial aid. A Level 7 in Mathematics opens doors to elite corporate bursaries and university scholarships that completely bypass the need for student debt.

Let us help you maximize your academic potential and clear the financial variables from your future. Explore our CAPS-aligned learning paths on our portal today!